Will Insurance Cover Your Roof? Age, ACV vs. RCV (NJ)

Does insurance cover your roof based on age? Many NJ policies flip from RCV to ACV at 10 to 15 years, so a 20-year roof's payout can be near zero.

Does insurance cover a roof based on age? It depends on one policy setting: replacement cost value (RCV) or actual cash value (ACV). Many NJ policies flip from RCV to ACV at 10 to 15 years. RCV pays a new roof minus your deductible; ACV depreciates it, so a 20-year-old roof can net near zero.

Updated July 2026 with the current NJ carrier roof-age rules, the exact policy line to read, and a payout-by-age table built from the ACV math we walk homeowners through on every storm inspection across Ocean and Monmouth County.

Every summer before hurricane season, we get the same call in Forked River, Toms River, Manahawkin, and up the Monmouth shore: "My roof is getting old, will insurance cover it if a storm hits?" The honest answer is that your roof's age has almost nothing to do with whether a claim is approved, and almost everything to do with how much money you actually see. That difference lives in two acronyms most homeowners never read on their policy until it is too late. I am Stephen Flury. Home Pro Remodeling is GAF Certified and has spent 20-plus years on Ocean and Monmouth County roofs, and this is the conversation I wish every homeowner had before the wind came, not after.

Does Insurance Cover a Roof Based on Its Age?

Whether insurance covers a roof based on age is really a question about how the payout is calculated, not whether the claim is denied. A covered peril is a covered peril: wind, hail, or a falling limb that damages a 22-year-old roof is just as covered as one that hits a 3-year-old roof. What age changes is the settlement method. Newer roofs typically settle at replacement cost value. Older roofs, on a growing number of NJ policies, settle at actual cash value, which subtracts depreciation for every year the roof has aged. The roof is covered. The check is a fraction of what you expected.

The reason this catches people is that nobody reads the loss-settlement terms when the policy renews. You see the premium, you see the dwelling coverage limit, you pay it. Buried in the declarations is whether your roof is insured for what a new one costs or for what your old one is "worth" after depreciation. On the Jersey Shore, where carriers have paid out heavily on wind and coastal claims, more policies are quietly moving roofs over 10 to 15 years old onto ACV at renewal.

RCV vs. ACV: What Is the Difference in Plain English?

Replacement cost value pays what it costs to put a new roof on today; actual cash value pays that same number minus depreciation for the roof's age and wear. That one subtraction is the whole story. On RCV, your only out-of-pocket cost is your deductible. On ACV, you pay the deductible plus every dollar of depreciation the carrier assigns, and on an older roof that depreciation can swallow most of the claim.

| Factor | RCV (Replacement Cost Value) | ACV (Actual Cash Value) |

|---|---|---|

| What it pays | Full cost of a new roof at today's prices | New-roof cost minus depreciation for age and wear |

| Your out-of-pocket cost | Deductible only | Deductible plus all assigned depreciation |

| Effect of roof age | None. Age does not reduce the payout. | Payout shrinks every year the roof ages |

| Who gets put on it | Newer roofs, or policies that never switched | Roofs past 10 to 15 years on many NJ policies |

| On a 20-year-old roof | New roof minus your deductible | Often near zero after depreciation and deductible |

Some policies split the difference with recoverable depreciation. The carrier pays the ACV amount up front, holds back the depreciation, and releases the rest once the work is completed and final invoices are submitted, usually within a 180-day to 2-year window. That structure is normal on RCV policies. The trap is a pure ACV roof endorsement, where the depreciation is never recoverable at all. What you get in the first check is all you get.

How Much Does an Aging Roof Actually Pay?

An aging roof on ACV pays less every single year, and the drop is steep enough to change what you should do about your roof today. Carriers depreciate an asphalt shingle roof against an assumed service life of roughly 25 years, most commonly on a straight-line schedule of about 4 percent per year. Run that against a real replacement number and the payout curve gets ugly fast. Here is the math on an $18,000 replacement (a typical two-story Ocean County job) with a $2,000 wind deductible.

| Roof age | Assumed depreciation | ACV payout (before deductible) | Net check after $2,000 deductible |

|---|---|---|---|

| 5 years | ~20% | ~$14,400 | ~$12,400 |

| 10 years | ~40% | ~$10,800 | ~$8,800 |

| 15 years | ~60% | ~$7,200 | ~$5,200 |

| 20 years | ~80% | ~$3,600 | ~$1,600 |

| 25+ years | ~95–100% | ~$0–$900 | $0 |

These are illustrative straight-line numbers and every carrier's schedule differs, but the shape is real and it is why a 15-year-old roof "might net 40 percent" while a 20-year-old ACV roof "can pay near zero." At 20 years, the depreciated payout barely clears the deductible. At 25, the deductible eats the whole thing and you write the check for the entire roof yourself, having paid premiums the whole time. That is not a denied claim. That is a covered claim that pays nothing, which feels worse.

What Is the One Policy Line to Read Before a Storm?

Read the Loss Settlement provision under Section I Property Coverage A on your declarations page, and any endorsement with "roof" in the title. That single clause tells you whether your roof settles at replacement cost or actual cash value. If it says "replacement cost," you are covered for a new roof minus your deductible regardless of age. If it says "actual cash value," "ACV," or references a roof payment schedule, your roof is being depreciated by age and you need to know that today, not after a nor'easter.

The specific things to hunt for on the declarations page and endorsement list:

- "Loss Settlement: Replacement Cost" vs. "Actual Cash Value." This is the master switch. It usually sits in the same block as your Coverage A dwelling limit.

- A "Roof Surfacing" or "Windstorm or Hail Losses to Roof Surfacing" endorsement. More NJ carriers are attaching this. It carves the roof out of your normal RCV settlement and drops it onto a depreciation schedule even when the rest of the house stays on replacement cost.

- A "roof payment schedule" or "roof age" table. Some policies now spell out the exact percentage they pay by roof age. If you see a table that steps down from 100 percent to 40 percent to 25 percent, that is the depreciation you will eat on a claim.

- Your wind or hail deductible. On the shore this is often a percentage (1 to 5 percent of the dwelling limit), not a flat dollar amount. On a $500,000 dwelling a 2 percent wind deductible is $10,000 before the carrier pays a cent, and on an ACV roof that can mean the claim never pays.

If you cannot find these lines or cannot tell what they mean, call your agent and ask one question: "Is my roof insured on replacement cost or actual cash value, and at what age does that change?" Get the answer in writing. That email is worth more than any inspection when a storm actually hits. For how the RCV and ACV numbers play out once a claim is open, our NJ roof storm damage claim guide walks the adjuster meeting and the supplement process line by line.

What Should NJ Shore Homeowners Do Before Hurricane Season?

Document your roof's condition now, before hurricane season, while it is intact and undamaged. The single most valuable thing an Ocean or Monmouth County homeowner can do is create a dated record that the roof was sound before the storm, because the fight on an aging-roof claim is almost always "storm damage" versus "pre-existing wear," and the homeowner who can prove condition wins that fight. Salt air, sustained coastal wind, and UV age a shore roof faster than an inland one, so barrier-island and bayfront homeowners have the most to protect here.

The pre-season documentation routine we give every homeowner:

- Pull the declarations page and read the Loss Settlement line. Know whether you are RCV or ACV, and at what roof age the switch happens, before anything is on the line.

- Photograph every slope, dated. Ground shots of each elevation plus close-ups of ridge, valleys, and flashing. A phone timestamp is enough. Store them somewhere you will find them in October.

- Get a dated written inspection. A licensed roofer's written report with photos, stating the roof was intact and functional on that date, is the record that separates a storm claim from a wear denial. Home Pro does this free across Ocean and Monmouth County.

- Write down the install year and shingle line. If you know the roof went on in 2008 with a specific shingle, that anchors the age argument and the matching-shingle argument later.

- Decide your move before the storm. If you are already on ACV and the roof is past 18 years, running the numbers now beats scrambling after the wind.

If you want the full pre-season checklist beyond the insurance angle, our Jersey Shore hurricane season roof prep guide covers the physical hardening (fasteners, flashing, gutters, projectiles) that actually keeps a roof on in a coastal storm.

When Does Replacing Before the Claim Beat Fighting Depreciation?

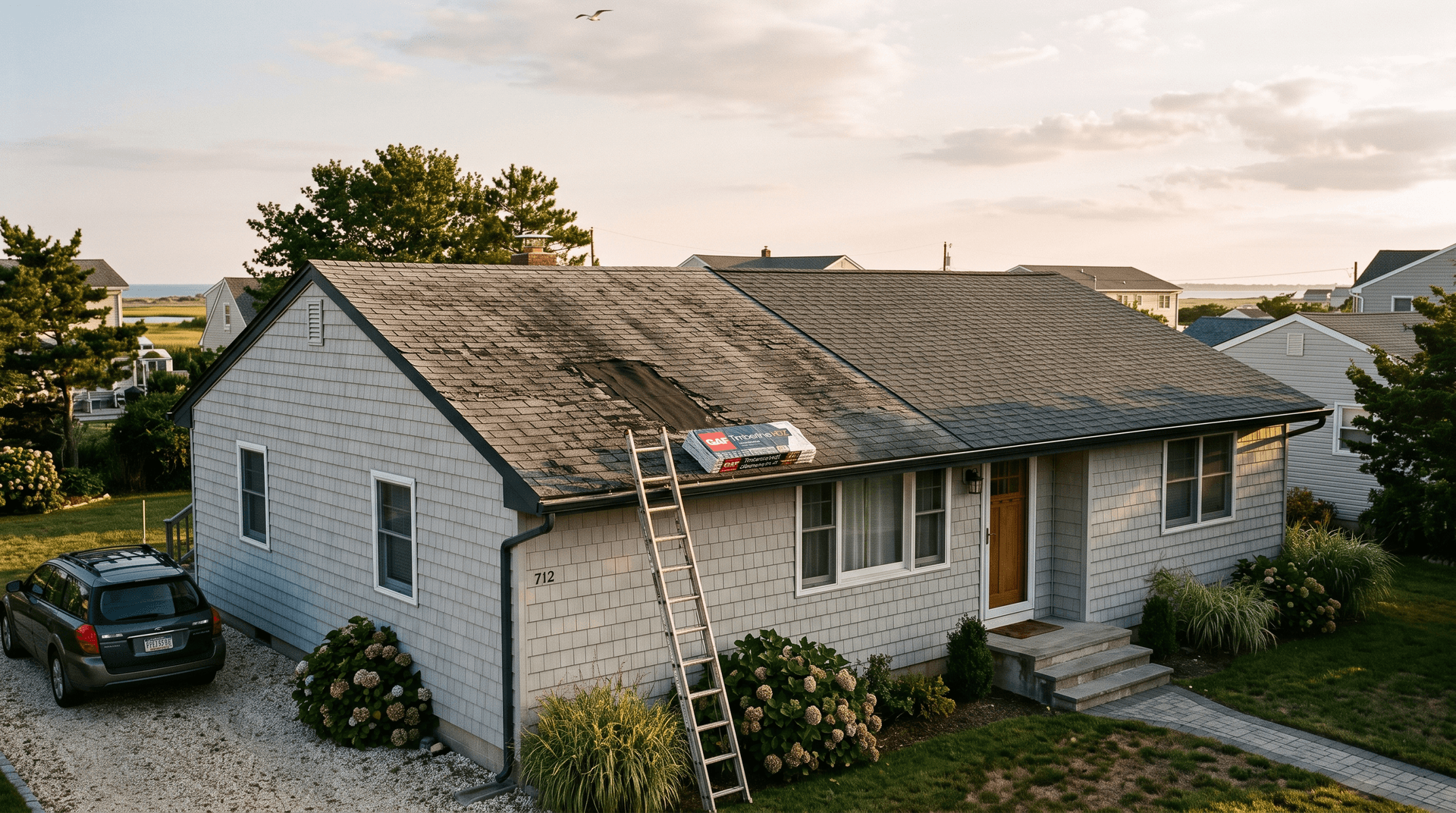

Replacing ahead of a claim wins when your roof is already on ACV, past about 18 years, and showing wear, because the depreciated payout you would fight for is worth less than the roof you are trying to save. Think about the 20-year-old roof in the table above. On ACV, a wind claim nets roughly $1,600 after the deductible. You still have a 20-year-old roof with two years of life left, and the carrier now has a wind claim on your record. Compare that to replacing it on your own schedule with a new GAF Timberline HDZ system that resets the clock, carries a 50-year material warranty and our 10-year workmanship guarantee, and often earns a premium credit for being a new roof.

The honest decision logic we run with homeowners:

- RCV policy, any age: do not pre-empt. If a storm hits, you get a new roof minus your deductible. Let the coverage work.

- ACV policy, roof under 12 years: usually still worth claiming after real damage, because depreciation is light and the net check is meaningful.

- ACV policy, roof 15 to 20 years and worn: this is the decision zone. The depreciated payout is small and the roof is near end of life. Replacing before the claim, on your terms, is frequently the better financial call, and a new roof can move you back toward RCV and a lower premium.

- ACV policy, roof over 22 years on original shingles: the claim will pay close to nothing. Budget the replacement as a homeowner expense, not an insurance event, and time it before the next storm forces the issue.

None of this means insurance is a scam or that you skip filing a real storm claim. It means you should know which side of the RCV/ACV line you are on before you decide, so you are making a money decision with the numbers in front of you instead of finding out at the adjuster's meeting. If you are weighing the cost of getting ahead of it, our Ocean County roof replacement cost guide breaks down every line item in a real replacement number, and our roof replacement and roof repair pages lay out exactly what our crews install.

Get an Honest, Documented Read on Your Roof

Home Pro gives every Ocean and Monmouth County homeowner a free roof inspection with a written, dated report you can hold onto for insurance: 20-plus years of shore roofs, GAF Certified installation, and a straight answer about whether your roof is worth claiming or worth replacing before the depreciation clock runs out. We walk the roof or fly a drone if it is not safe to climb, check the deck and ventilation from the attic, and tell you where you actually stand. Call (732) 703-7808 or request an inspection through the contact page and we will be on the property within 48 hours across Forked River, Lacey, Bayville, Barnegat, Manahawkin, Toms River, Brick, Waretown, Berkeley, Tuckerton, the LBI corridor, Howell, Wall, Manasquan, Brielle, Spring Lake, Sea Girt, and anywhere else in Ocean or Monmouth County. Document the roof now, before hurricane season writes the story for you.